Hawaii General Excise Tax Registration After LLC Formation in 2026: What New Owners Miss

Hawaii general excise tax registration is the first Hawaii Department of Taxation filing a new LLC needs to clear before the first dollar of revenue hits the books. You formed the LLC. You signed the operating agreement. You opened the bank account. You are ready to invoice the first client. Then the Hawaii Department of Taxation sends a notice asking why no Form BB-1 has been filed, and you realize that forming the LLC and registering for Hawaii’s General Excise Tax are two different filings with two different agencies. Most new owners do not realize that Hawaii’s General Excise Tax (GET) is a tax on gross receipts at the entity level, not a state sales tax on the consumer. The filing obligation starts the moment the LLC earns income from activity in Hawaii — sometimes even earlier than the owner expects. Here is what new owners miss, and the practical order for getting it right the first time.

Here is the broader picture on registered-agent costs and what most owners underestimate when they form an LLC:

What the Hawaii General Excise Tax license covers

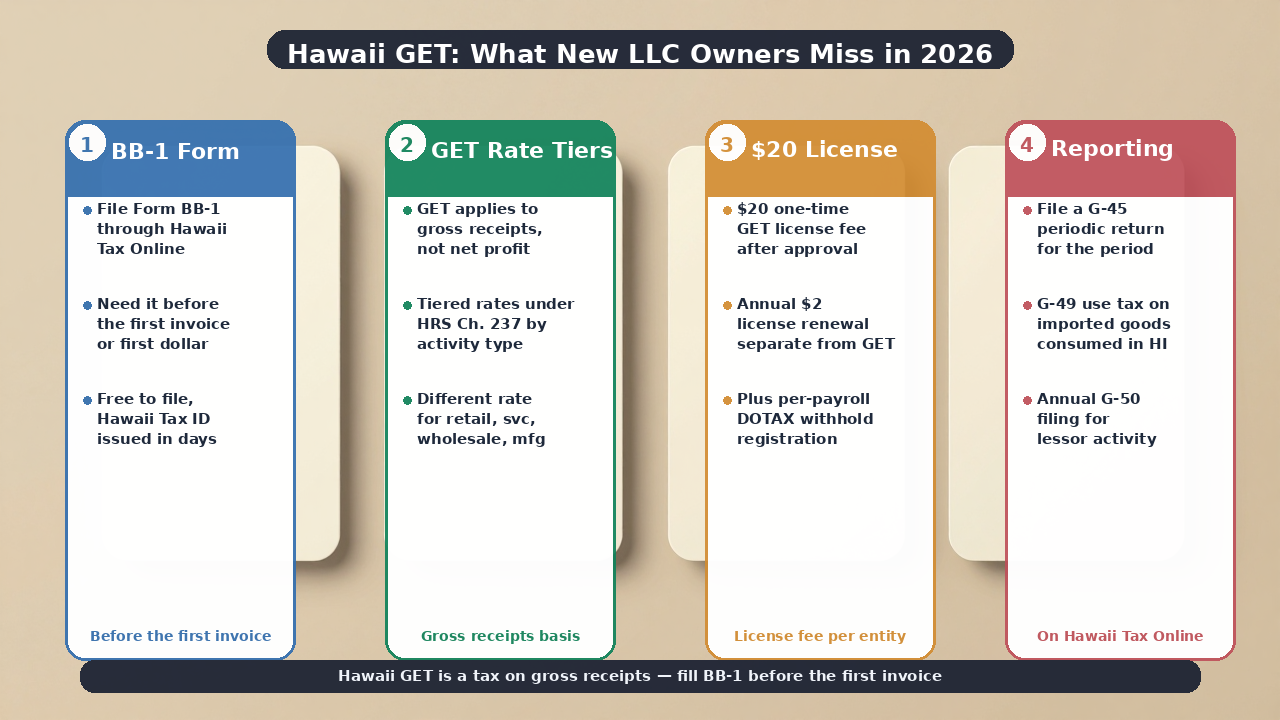

The Hawaii GET license is the operating permit that authorizes the LLC to engage in business activity in Hawaii and to collect the General Excise Tax on gross receipts from that activity. The license is issued by the Hawaii Department of Taxation (DOTAX) under Hawaii Revised Statutes Chapter 237. The license is required for every Hawaii LLC that engages in business activity in the state — including activity by out-of-state LLCs that meet the economic-nexus threshold under Hawaii Tax Online account registration. The LLC ends up with a Hawaii Tax ID (the DOTAX taxpayer account number) that the LLC uses on every state tax filing from that point forward — GET returns, Use Tax returns, withholding returns, and corporate or partnership filings if the LLC is later converted.

The $20 one-time license fee

Under Hawaii Tax Online, and the $20 fee is paid by credit card or ACH at the time of submission. Paper filings require a check or money order attached to Form BB-1 Rev. 2025, the State of Hawaii Basic Business Application.

What the Hawaii Tax ID is and is not

The Hawaii Tax ID is the DOTAX-issued taxpayer account number that the LLC receives when the Form BB-1 is processed. The Hawaii Tax ID is the anchor identifier for every Hawaii state-level tax filing the LLC will ever make. The Hawaii Tax ID is not the federal EIN. The federal EIN is issued by the IRS. The Hawaii Tax ID is a separate identifier issued by DOTAX. The LLC needs to track both numbers separately and use the correct one on each filing. The Hawaii Tax ID is not the same as the LLC’s Department of Commerce and Consumer Affairs (DCCA) business registration number. DCCA registers the LLC at formation. DOTAX registers the LLC for tax purposes at GET licensing. Two different agencies, two different identifiers. The Hawaii Tax ID becomes the identifier the LLC uses to file Form G-45 (the periodic GET return), Form G-49 (the Use Tax return), Form HW-14 (the withholding return), and Form N-1 or N-3 (the corporate or partnership return) — every Hawaii tax return runs on the same Hawaii Tax ID.

The GET rate tiers under HRS Chapter 237

Under The wholesaler typically buys inventory from a manufacturer or importer and resells it to a retailer or another wholesaler. The service rate is the same as the retail rate. A consulting LLC, a landscaping LLC, or a software LLC all pay 4.5% on their gross service receipts. Insurance and pass-through real estate carry their own tiers. Insurance is The four things new Hawaii LLC owners most often miss The pattern that comes up again and again in 2026: The statutory deadline under Hawaii Department of Taxation processes the BB-1 typically within one to three business days for online filings, so filing early is essentially free. The LLC gets the rate wrong because it does not understand that GET applies at the entity level on gross receipts, not at the consumer level like a sales tax. An LLC expecting to deduct COGS first is in for a surprise. The tax is on what comes in, not on what is left after expenses. Hawaii has a Use Tax that mirrors GET and applies on imports of goods that escape the GET. The Use Tax is collected on Form G-49 alongside Form G-45. An LLC with inventory purchases from out-of-state vendors owes Use Tax on those purchases if the vendor did not collect Hawaii’s equivalent. The LLC misses the economic-nexus threshold under How the LLC files Form BB-1 in 2026 The filing path goes through Hawaii Tax Online. The account requires the federal EIN, the LLC’s legal name, the principal address, and a contact email. The account is tied to the responsible party — the LLC member or manager who controls the entity. The form is the State of Hawaii Basic Business Application, and it covers the GET license, the Hawaii Tax ID assignment, and any ancillary registrations the LLC needs (withholding, transient accommodations, fuel, etc.). The same form covers multiple registrations so the LLC does not have to file a separate application for each tax type. Online submissions are confirmed immediately. The Hawaii Tax ID is assigned when the application is approved — typically within one to three business days for online filings. The G-45 is the periodic General Excise Tax return. The filing frequency depends on expected liability. Most new LLCs start as semi-annual filers. For paper filings, the LLC uses Form BB-1 Rev. 2025, downloaded from the DOTAX forms page. Paper filings take longer to process than online — typically 4 to 6 weeks. The GET license is one of three Hawaii state agencies a typical LLC works with. The other two are the Department of Commerce and Consumer Affairs (DCCA) and the Department of Labor. DCCA handles business registration at formation. The LLC’s articles of organization and annual filings (covered in the Hawaii Annual Report Rules for LLCs and Corporations in 2026) run through DCCA. DCCA is the LLC’s formation agency. DOTAX is the LLC’s tax agency. The Department of Labor handles the LLC’s unemployment insurance registration if the LLC hires employees. The Department of Labor registration is separate from the GET license. The LLC needs both if the LLC has W-2 employees. Trade-name registration for the LLC’s DBA also runs through DCCA and shows up in Form BB-1 line 5. The Hawaii Trade Name vs LLC Name: 2026 Filing Rules for Small Businesses article covers how the trade-name line interacts with the LLC name on the articles of organization. For the full set of state-level documents the LLC will interact with, the Real Documents You’ll Need for a Hawaii LLC guide covers the LLC’s documents set alongside the Hawaii general excise tax registration. If a Hawaii LLC wants the broader compliance picture across registered-agent duties, exemptions, and what filings are actually required, this walkthrough covers the cycle: DOTAX treats a late Form BB-1 as a back-tax situation, not just a paperwork fix. The LLC owes the GET that would have been due from the moment business activity began, plus interest, plus late-filing penalties. For a service LLC that quietly ran for six months before registering, the back-tax bill can reach 4.5% of six months of gross receipts — often more than the LLC’s net profit for the period. The penalty structure under HRS Chapter 237 is layered. There is a percentage-based penalty on the unpaid tax, plus interest at the underpayment rate, plus a separate failure-to-file penalty if the periodic G-45 returns were never filed. For an LLC that discovers the omission on its own, voluntary disclosure through DOTAX typically cuts the penalty exposure significantly compared to waiting for DOTAX to send the notice. For an LLC that has already received the notice, the practical path is to file the BB-1 immediately, file the missing G-45 returns, pay the back tax plus interest, and ask DOTAX about penalty abatement based on the LLC’s clean compliance history. The first-time-penalty abatement is granted more often for LLCs that self-correct than for LLCs that wait for the notice and then respond. The practical rule for a new Hawaii LLC in 2026 is to file Form BB-1 through Hawaii Tax Online the moment the LLC begins business activity in Hawaii. Do not wait for revenue. Do not wait for an accountant. Do not assume the DCCA formation filing covers the tax registration. The DCCA formation and the DOTAX registration are two separate filings with two separate agencies. Pick the right GET rate tier on the BB-1 submission. Default to 4.5% for services and retail if the LLC is unsure, then amend through Form BB-1 with the correct rate if the actual activity is different. The $20 one-time fee is the cheapest step in the LLC’s tax life — every subsequent correction costs more. Treat the Hawaii general excise tax registration as the LLC’s first DOTAX obligation rather than its only one. Withholding registration for employees, Use Tax compliance for inventory from out-of-state vendors, and economic-nexus registration for out-of-state LLCs doing business in Hawaii all flow from the same Hawaii Tax ID. For an LLC that wants the Form BB-1 filed, the right rate selected, and the Hawaii Tax ID put into service so the LLC can invoice the first client — typically when the LLC is freshly formed or expanding from no revenue to first contracts — start a Hawaii general excise tax registration through Rapid Registered Agent. That is the whole job of Hawaii general excise tax registration in 2026 — and now you know how to clear it before the first invoice goes out. Before you scroll to the FAQ, here are the registered-agent FAQ answers most LLC owners hit next: The Hawaii general excise tax registration is the filing an LLC submits to the Hawaii Department of Taxation (DOTAX) to obtain a GET license and a Hawaii Tax ID. The registration is Form BB-1, the State of Hawaii Basic Business Application, and is required for every Hawaii LLC that engages in business activity in the state under HRS Chapter 237. The Hawaii GET license costs a one-time $20 fee under HRS § 237-16. There is no annual renewal fee for the license itself. The fee is paid as part of the Form BB-1 submission through Hawaii Tax Online at hitax.hawaii.gov or by mail using Form BB-1 Rev. 2025. Under HRS § 237-13, the four primary GET rate tiers are: 0.5% on wholesaling of tangible goods for resale, 4.5% on retail sales to end consumers, 4.5% on services performed in Hawaii, and 0.5% on manufacturing. Insurance is 0.15%. Pass-through real estate is 0.5% under Act 18 SLH 2024. A Hawaii LLC must file Form BB-1 before engaging in business activity in Hawaii. The statutory deadline is the moment the LLC begins operations in the state. Many new owners file late because they treat the GET license as a revenue trigger rather than an activity trigger, then owe back taxes plus penalties once DOTAX catches up. No. Hawaii’s GET is a tax on gross receipts at the entity level, not a sales tax on the consumer. The tax applies to what comes in regardless of expenses, and the LLC owes GET even when it is operating at a loss. The LLC cannot deduct COGS before calculating GET the way it can for income tax. Yes, if the out-of-state LLC meets the economic-nexus threshold under HRS § 237-8.5 — $100,000 or more in Hawaii gross receipts, or 200 or more separate Hawaii transactions, in the current or previous calendar year. The LLC must register with DOTAX, obtain a Hawaii Tax ID, and pay GET on Hawaii-source receipts.The LLC waits too long to file Form BB-1

The LLC gets the rate wrong

The LLC forgets the Use Tax companion rule

The LLC misses the economic-nexus threshold

The relationship between the GET license and the LLC’s other Hawaii state filings

What happens if the LLC files BB-1 late

The practical rule for 2026

Related reading

Frequently Asked Questions

What is the Hawaii general excise tax registration?

How much does a Hawaii GET license cost in 2026?

What are the Hawaii GET rate tiers?

When does a Hawaii LLC need to file Form BB-1?

Is the Hawaii GET the same as a sales tax?

Does an out-of-state LLC need a Hawaii GET registration?